Buying or converting a property into a HMO can be hugely profitable — but only if you stay on the right side of the planning system.

One of the most common questions investors ask me is:

“When does a HMO actually need planning permission?”

It sounds like a simple question, but sadly it isn’t!

It all depends on permitted development rights, Article 4 directions, the so-called ten-year rule and local planning policies.

And, as I explained in a recent article, the planners are targeting HMO landlords more than they ever have before.

So here is a straightforward explanation — based on my many years of dealing with councils, appeals and enforcement cases across the country.

First things first: What is a HMO?

A House in Multiple Occupation (HMO) is a property lived in by three or more people who form more than one household and share facilities such as a kitchen or bathroom.

They can range from small shared houses with a few unrelated tenants to larger, more intensive arrangements with many occupants.

Planning law, licensing rules and local policies all use slightly different definitions, which is part of what makes HMO regulation so confusing for investors.

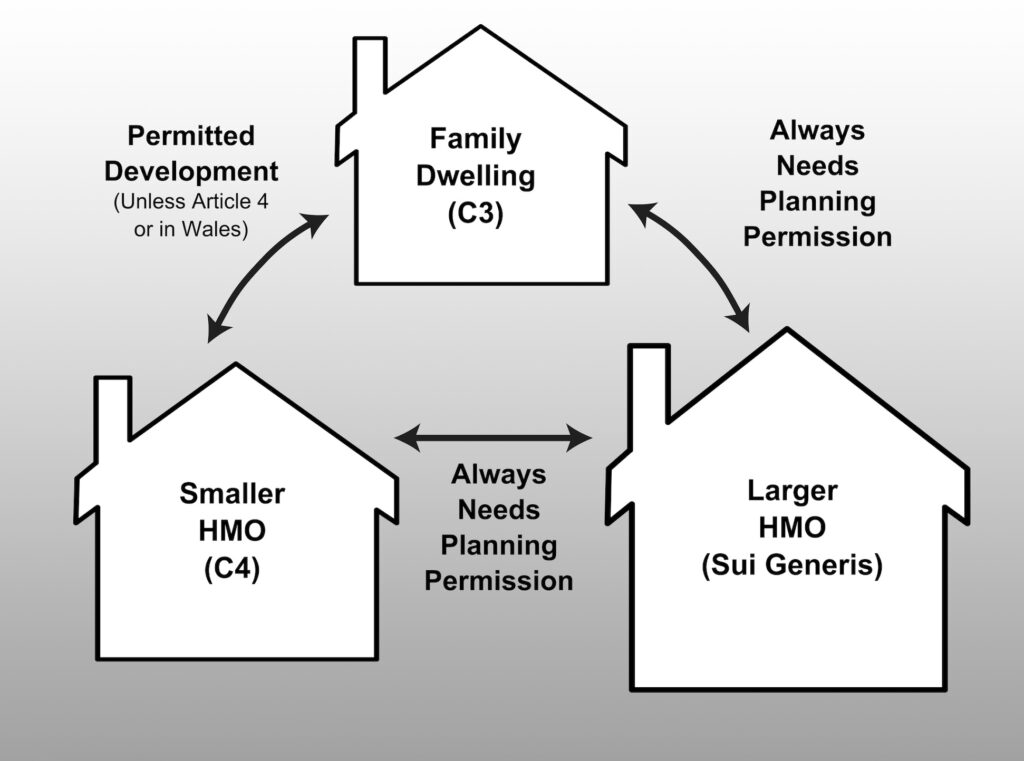

C3, C4 and Sui Generis: the basics

Every property sits within a “use class”. For HMOs the key ones are:

- C3 – a normal dwellinghouse (single family).

- C4 – a small HMO (3–6 unrelated occupants).

- Sui Generis – larger HMOs (typically 7+ people) or anything unusual that doesn’t fit a class.

Generally speaking, you need planning permission to change from one use class to another (because it is a change of use). However, changes between C3 and C4 are permitted development, meaning planning permission is not required.

The C3 → C4 change is permitted development… unless it isn’t

Under national rules, changing from a normal house (C3) to a small HMO (C4) is permitted development, meaning you don’t need to apply for planning permission.

This is where many investors stop reading — and that’s when they get into trouble.

Because councils have a powerful tool up their sleeve…

Article 4 directions remove permitted development rights

A council can issue an Article 4 direction to remove the automatic right to convert C3 → C4.

And many councils have done exactly that.

In an Article 4 area:

- A C3 → C4 change does need full planning permission.

- A 7+ person HMO (sui generis) always needs planning permission.

- Councils can refuse applications on grounds such as over-concentration, parking, amenity and character.

Investors who assume permitted development applies everywhere often find themselves facing enforcement notices, retrospective applications — or appeals.

Just 3 people is enough to create a HMO

It is commonly assumed that HMOs must be larger shared homes, perhaps with 6 or more people.

In fact, planning law defines a HMO as any home with 3 or more people living in 2 or more households.

If you rent a two-bedroom flat to a couple and one other individual, you have created a HMO. If you are in an Article 4 area, that HMO is not permitted development and required planning permission.

What about a HMO that has been operating for years?

If a property has operated as a HMO continuously for ten years, it may be lawful — even if it never had planning permission.

But proving ten years of continuous use is hard.

Councils require:

- tenancy agreements

- council tax or utility evidence

- sworn statements

- inspections or licensing records

And any gap in evidence can reset the clock.

So when do you actually need HMO planning permission?

You need planning permission for a HMO if:

- You’re in an Article 4 area and want to convert C3 → C4

- You’re creating a sui generis HMO (7+ people)

- You can’t prove ten years of continuous HMO use

Final thoughts

HMOs remain one of the best investment strategies in the UK — but only if you understand the planning challenges.

Councils are much more alert to HMOs than they used to be: Article 4 directions are widespread, and planning refusals and enforcement investigations are common.

If you’re planning a new HMO or you’re worried about an existing one, get advice early.

It saves a lot of money and a lot of grief.

Read all about it!

For a deeper dive into getting planning permission for HMOs, take a look at my book, Planning for HMOs: A Practical Guide to Planning Permission for Houses in Multiple Occupation.

It sets out, in plain English, everything landlords need to know about planning rules, Article 4 Directions, Certificates of Lawfulness and enforcement.

Whether you already run HMOs or you’re planning your first conversion, it’s full of real-world examples, practical tips and insights gathered from years of helping landlords navigate the planning system.

Available now at www.martingaine.com/hmos.